CRNAs: Financially Independent within 10 Years

Bold statement to say a CRNA won’t need earned income 10 years after graduation, but it’s possible. Not just possible, realistic. One of my biggest pet peeves is when folks making insane amounts of money complain about not having any. I'm about to run through case study showing you just how easy it is for the average earning CRNA to retire just 10 years out of school.

Statistics vary, but the average CRNA earns an annual gross income of $203,000.

I found a nice article on CNBC stating middle class incomes in the United States range from $41,000 annually to $141,000 annually. Sure, there are some urban and beachfront areas where $200,000 puts you at the top of the middle class, but that's a rarity.

As you move out of desirable populated areas, the middle-class income shifts to the left. This means half of the annual CRNA salary would put you at the top of the middle-income category.

I say this to bring perspective we continue.

I will craft an example using J, a fictitious 30-year-old new grad CRNA. J makes and spends averagely. Nothing exciting here.

Income

Operating on multiple assumptions here, but J makes just over $200,000 as a W2 employee filing as a single taxpayer. He brings home approximately $145,000 annually. Let’s call it 12,000 per month.

Perks

$25,000 sign on bonus paid up front for a 3-year commitment. 3% employer 401(k) match. HSA is offered. Some benefits are included in the benefits package, but J pays for health insurance, which is accounted for in the monthly expenses listed below.

Student Loans

I wasn’t able to find solid data on average CRNA student loan debt, but to keep all things reasonable, let’s assume J carries $150,000 in student loans at a 5% interest rate. No other debt. No other savings.

If carried out over a 10-year term, the monthly payment would be $1,600.

Cost of living

I explored the United States Bureau of Labor statistics website and came across there 2021 consumer expenditure survey, which provided much of the following data.

I understand this is not real-time, July 2023 data, but it takes a significant amount of time and energy to gather data on a national scale, so this is the most current data available.

The national average expenses for a single [individual] in the United States is $3,400 per month. The average household net income for single households is $39,000. J is looking rather outstanding thus far with his $145,000 net income.

About $1,400 goes towards housing and utilities. Reasonable to rent a small place in much of the United States. I can only account for so many assumptions, so this is what I’m going with.

Assumptions

Cost of living and pay both increase 3% annually. J owns a cheap 15-year-old car that reasonably transports him to work.

J chooses to rent as this is his first job and doesn’t want the commitment and hassle of buying. Plus, he is broke. J’s financial goals are to become financially independent with middle class comforts.

Note: It is more expensive per person to live alone as opposed to a couple who can share costs such as housing, utilities, and internet. I’ll give an example of this as well.

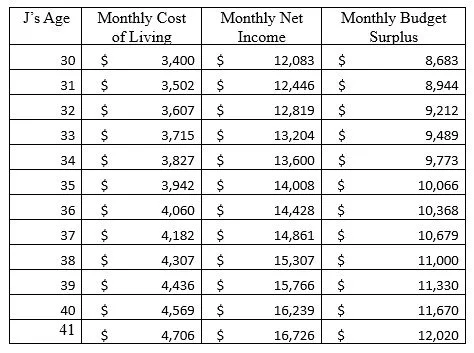

Let the charts begin…

This is a general overview of what J’s income looks like with the average cost of living in the United States:

Where does J start?

TFC Digression: Lifestyle is dictated by net worth, NOT by income. J is broke.

It’s a good thing J reads The Financial Cocktail, so he knows exactly where to start. Because he carries a bunch of debt at a fairly high interest rate, he understands living like an SRNA for a while longer is ultimately a strong financial course of action.

You read that correctly, J has $8,683 to work after paying his living expenses EACH MONTH. Almost $100,000 annually!

He starts by building an emergency fund of $1,000-$2,000 that he holds in a money market account. This account has a variable rate but is likely paying 4-5% at this time. He can set aside this money from the $25,000 sign-on bonus or from his first paycheck.

Interest on the student loans after just one year is minimal, so I will calculate the repayment based off the original $150k amount. J can pay off his student loans in less than 18 months.

Let’s assume J wants to take advantage of the employer 401(k) match, which is a mathematically strong move. J would apply 500 pretax dollars towards the account each month. He can make this investment AND pay off his loans in 18 months.

Note this chart doesn’t account for using any of the sign-on bonus for loan repayment. J could absolutely outpace this chart.

Debt Free

Big milestone here. One that should be praised and celebrated. It’s absolutely doable in a short amount of time with a CRNA income. And these numbers didn’t include extra income. Simply the average CRNA compensation.

Unpopular Opinion: I hear a lot of excuses as to why 10+ year CRNAs have student loans and they are all BS.

J’s next move is to expand the emergency fund to cover 3-6 month’s expenses. His monthly cost of living is $3,500 so $10,000-$20,000 is a great range to have in that money market account.

This is enough to cover most medical bills, transportation issues, and the loss of employment. Really a security blanket that allows him to sleep well at night. Despite J’s net worth being just north of $0, J’s personal financial status is years ahead of the average 31-year-old.

Every financial advisor would gawk at this situation and wish you were their client because they would make so much money off you. I can speak to this first hand.

Financial Independence (FI) Number

One’s FI number is based off the annual cost of living. It assumes a 4% annual withdrawal from the portfolio to sustain the desired standard of living without any additional earned income. Read more about it here.

J may look to calculate his estimated cost of living off $5,000, which should cover a similar cost of living 10 years down the road. Reference the previous chart.

FI Number = $5,000 x 12 months x 25 = $1.5M

J can invest with the goal of having a $1.5M nest egg to retire in his early 40s.

Wealth Building

J has a goal, now how to get there? -- Consistent investing and tax management

J is shooting for that 10-year mark of age 40. This equates to a monthly investment of $10,000 to reach $1.5M.

Yes, J would need to increase his income to meet this goal. He is compensating by utilizing tax advantaged accounts which decrease his tax burden greater than mentioned above. He has an employer match. He could also compensate by increasing his monthly investments as his income increases. But for simplicity, J will invest a flat amount each month for the duration of his working career.

Tax Advantaged Accounts

He transitions to the wealth accumulation phase. It’s time to make use of tax advantaged accounts available through the United States tax code.

J can invest $22,500 annually into his employer sponsored 401(k). This is a pretax contribution, so it lowers taxable income. His employER contributes $6,000 annually due to the 3% match.

J can also contribute $3,850 to a health savings account. Also, a pretax contribution. There are other places to invest, but these are two big ones that allow for a $26,350 deduction from J’s taxable income.

The contribution amount for these accounts typically increases year after year, but let’s assume it doesn’t. And J contributes the maximum amount, which is almost $2,200 per month. I will assume an 8% annual return.

Accounting for 10 years of inflation adjusted wages, J will be making almost $300,000 annually at the same job. So, $2,200 per month is minimal. His investments will go up as it becomes a smaller and smaller portion of his income, but let’s assume the worse.

If J ONLY invests in his retirement accounts, he will be a 401(k) millionaire by age 50.

At age 31.5, J has contributed $9,000 to his 401(k) to meet the employer match of $9,000. Now he contributes $2,200 per month into the various retirement accounts. At age 40, his account will be worth $352K. If he invests for an additional 10 years, his half centurion value will be $1.2M.

The 401(k) and pension millionaires make up a great deal of well-off retirees making average or just above average incomes. Think teachers, engineers, and union workers.

Just for kicks…

Making the radical assumption that J continues with the median cost of living from age 31.5 to age 40 AND he invests the surplus income, what will that look like? Assuming a flat monthly investment of $8,000 with an annual return of 8%, J’s investments will total $1.3M between his tax advantaged accounts, employer match, and other investments.

If J continues investing this way, he will have amassed $2.5M by age 45.

Keep in mind that his cost of living will grow year after year. I realize this alters the FI number, but he continues to live on half of his NET income. Note the growing difference between “monthly net income” and $8,000.

This supports J increasing his standard of living, which is to be expected.

So, become a CRNA at age 30 with no money to your name and $150,000 in debt and you can become a millionaire with the average CRNA salary within 10 years. No overtime required.

I would question why J doesn’t have any savings after presumably working for nearly a decade prior to starting anesthesia school. I would also look into a more affordable education experience. I paid for CRNA school with 2.5 years of nursing in one of the lowest paying states. Regardless, I feel this case study is applicable.

What if J had a spouse?

Great question. Per the U.S Bureau of Labor Statistics, average household monthly expenses would increase from $3,400 to $5,500. This also comes with the assumption that the spouse also contributes to the income.

Two incomes allow for double the pretax contributions. It also lowers the tax bracket, even if the spouse doesn’t work. At the end of the day, J and his spouse would be able to make better progress together.

Yep, the timeline would actually be shorter! – Provided the spouse doesn’t come with a plague of money troubles, massive debt, or an extremely low paying career. All great things to talk about pre-marriage.

If J’s spouse made the difference in cost of living ($2,100 per month), they would actually be ahead financially considering the tax advantages. And no, I don’t recommend marriage nor children for the tax incentives. I know someone is thinking that.

Factors that accelerate the timeline.

Increase your income -- Pretty obvious. This is my one leg of my multifactorial approach. It allows me to plant seeds of the money tree earlier. There is absolutely a risk of burning out, but the upside is that I accelerate my portfolio early and allow compound interest to fully support my cost of living more quickly.

If J picked up a shift or two per month, that would allow for a significant income increase while maintaining his cost of living. This would allow J to even more aggressively pay off his debt.

Extra shifts are where Mrs. TFC and I come up with money for things like vehicles and houses. We don’t interrupt the monthly investment amount. Ever. For anything. Ever.

Increase annual return. Look at the massive difference that results with a small change in annual return. Assume conservatively when you are calculating how much you will need for retirement.

This is where some venture into real estate looking to increase their returns and lower tax liability. Valid approach. Be mindful of the additional time and effort needed to manage such an investment.

Factors prolonging the timeline

Poor attitude. I read this awesome book by Jacko Willink and Leif Babin titled, Extreme Ownership: How U.S. Navy SEALs Lead and Win. It’s about being honest with yourself and understanding you are never exempt from every degree of fault.

Everyone’s hand holds some unfortunate cards and mine is no different. There are an infinite number of excuses out there as to why you aren’t succeeding financially with a CRNA income. Fault lies in the mirror. Really though, the book is great.

Entitlement. Like attitude, but this one bugs me more than anything. I just want to say that just because you are a CRNA making CRNA dollars doesn’t mean you are wealthy. It just means you make good money. If you are like J with student loans and debt, you don’t deserve a new house or new SUV. You don’t deserve an expensive vacation because you passed boards.

Congratulations on your accomplishments, but it’s not an excuse to spend irrationally.

Unfortunate life events. This absolutely prolongs the timeline. No doubt about it. Refer to Jacko’s book about what to do when these things happen.

It might mean you step away from work for a while. Maybe it means you pick up shifts to cover an unexpected breakdown. Were you as prepared as you could have been?

I sympathize and empathize with those who truly see the bad side of life’s curve balls. And you know what, if J cleans up his debt quickly, that 3-6 month emergency fund may negate the financial influence of these events.

The emotional aspect is another story, but everything is easier when you aren’t stressed about paying the bills. You can devote all of your energy to the crisis at hand.

What a depressing ending. I’m going to recap with the fact that the average CRNA can become financially independent and retire with middle class comfort within 10 years despite starting their gas passing career with mountains of student loans.

If you had the intentions of being like J, but can’t find a way around life’s barriers, reach out. TFC currently offers financial coaching. We become a team to conquer your financial aspirations.